by Thanos Pallis & George Vaggelas

Greek ports experience eventful times. While they have successfully managed to sustain operations in conditions of lockdowns and covid-related restrictions, the pandemic outbreak has been followed by severe disruptions and changes in maritime supply chains. Lines shipping itineraries and models for serving the global economy are revisited generating prospects and challenges.

Private operators and owners of the two major Greek ports, Piraeus and Thessaloniki, and public authorities responsible for the rest of the Greek port system have strived to benefit from the prospects generated, but also to address the related challenges.

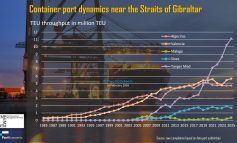

The epicenter of these efforts has been the increase of their presence in the international container port market. This is an effort to reverse the observed stagnation of the recent two years. A decade of growth, which reached a peak in 2019, has been followed by two successive years of decline due to the pandemic (2020-2021). Yet it is worth noting that the total throughput in 2021 is almost triple the respective total recorded ten years before.

What have Piraeus and Thessaloniki achieved?

The growth of container throughput in Greece is mainly attributed to the emerging dynamics in Piraeus since the assumption of its operations by an international terminal operator affiliated with one of the major liner shipping companies in the world (COSCO Shipping Ports Ltd). To a lesser, yet significant, extent, it is also attributed to the aftermath of the post-privatization era in Thessaloniki. However, what seems capable of enhancing their long-term prospects is the upgrades of the connectivity of both ports that integrate them into broader maritime networks.

In the latest five years (2017-2021), container throughput in Piraeus increased by 28,3% reaching 5.317 million TEUs. Piraeus is today the fifth biggest port in Europe and the third biggest (following Valencia and Tangier-Med) in the Mediterranean Sea. During the same period, Piraeus enhanced its embeddedness in the major shipping networks. In late 2021, 9% of the registered calls were vessels with a capacity between 12.500-18.000 TEUs, and 5% of the calls were vessels with a capacity of more than 18.000 TEUs. Since 2018 Piraeus has been facilitating containership vessels of over 20.000 TEUs capacity calls.

Piraeus connectivity has been upgraded. In 2022 it is a hub port connected directly with 72 ports in 30 countries. Seventeen (17) of these countries are in Europe, ten (10) in Asia, and three (3) in Africa. Direct services connect it with major world hub ports such as Singapore (21 itineraries per month), Port Klang in Malaysia (6 itineraries), Colombo in Sri Lanka (4 itineraries), Rotterdam (15 itineraries), and Antwerp (9 itineraries). Feeder vessels regularly serve ports in Turkey, Italy, Greece, Egypt, and Israel. All these highlights the role of Piraeus in the East Mediterranean region but also in geographically broader networks.

This port function is confirmed by the choice of all major liner shipping companies to call Piraeus. The port is attracting calls primarily from the members of the alliance in which its owner (COSCO) participates: approximately 40% of the calls are “Ocean Alliance” members. “2M” alliance vessels equal about 15%, while “The Alliance” vessels are also calling Piraeus. COSCO vessels call more frequently than any other shipping line (20% of total calls), followed by Hapag Lloyd and MSC, Evergreen, and CMA-CGM.

Similar have been the achievements in the case of the port of Thessaloniki. The connectivity of the port has increased remarkably. The number of countries directly linked with the port has increased by 62%, the number of ports directly connected with it has increased by over 53%, and the size of the capacity of the smaller vessel calling at Thessaloniki has doubled.

Thessaloniki is linked directly with 22 ports in 12 countries with feeders from/to Greece (30% of all calls) and Turkey (also 30%); Cyprus, Egypt, and Malta follow. Piraeus is the most popular call before or after Thessaloniki, followed by Limassol and Asyaport, one of the nine Turkish ports linked directly with the port. 36% of the calls are MSC vessels. The related to the port’s ownership (via Terminal Link), CMA-CGM is the other liner frequently calling at the port (19%), with COSCO και X-Press feeders being the other frequent callers at the ports.

This has been achieved even though, compared to 2019, neither the size of calling vessels nor the capacity of the biggest vessel calling at the port have changed. At the end of 2021, the average capacity of containerships calling Thessaloniki was 1.573 TEUs. Moreover, despite any advancements, infrastructure upgrades were still in the planning phase, and post-Panamax cranes were only delivered in May 2022. Yet, operational improvements and establishing the dry port in Sophia have enabled the Port of Thessaloniki to emerge as a more dynamic gateway port in the region.

The Prospects

The prospects of Greek ports are tied primarily to their capacity to successfully respond to the structural change in the container market in the Mediterranean and beyond, as recently reported in the IAPH World Port Tracker.

In the last year alone, the number of container vessel calls in Mediterranean ports decreased by -11,5%. At the same time, the share of containerships that are larger than 8.500 TEU capacity increased by 3,9%; among these largest vessels are the biggest containerships of all, which are deployed in the main East-West maritime services – with several ports in the region publicizing calls of vessels of more than 20.000 TEU capacity.

It is the increase in the size of calls, i.e., the number of containers (un)loaded per call, that reached record levels in 2021. Since early 2020, the average vessel calls at Mediterranean ports have been coupled with more containers handled per call in every quarter of the year than in early 2019. At the end of 2021, the average call size was 5.5% higher than in the same quarter of the year before. The growth is reflected in the calls resulting in the handling of 3.001-4.000 TEUs; in three years only (2019-2021), such calls increased by 25.9%. Calls (un)loading 4.001-6.000 TEUs are today more than double the number of calls in this category that occurred in early 2019. The growth has been even more impressive in the biggest calls, i.e., those of 6.000 TEU or more. At the end of 2021, the number of such calls in the Mediterranean ports was nine times more than in early 2019.

Despite these changes or disruptions in maritime supply chains, Mediterranean ports have improved their productivity, as reflected in the evolution of the port moves per hour. On a year-on-year basis, the port moves per hour at the end of 2021 were 3.5% more than at the beginning of 2019. Yet, in recent times productivity improvements seem to evaporate. Ports have to serve more cargoes per call in a more productive way.

Under these conditions, significant infrastructure upgrades in both Greek ports and increased capacity are essential. In Piraeus, in recent times, signs of congestion have been present, along with delays in certain parts of the investment program. Yet, discussions on developing a fourth pier for facilitating container traffic have started. Similarly, in Thessaloniki, the long-waited expansion of Pier 6 seems to advance.

A lot will depend on the capabilities of Greek ports to improve their efficiency and effectiveness. Operational improvements (including digitalization and effective serving of current and future uses), better monitoring of performance gaps, and further exploitation of hinterland connectivity to establish better supply chains (i.e., train connections, Thriasio distribution centre (Piraeus), the dry port in Skopje (Thessaloniki), the resolving pending labour disputes and, not least, the improvements in port-city relations, would all enable the major Greek ports to provide a better value proposition.

The progress of the ongoing privatization program – despite its peculiarities and potential negative effects resulting from them – might also provide more options to potential users. Alexandroupoli, Heraklion, and Igoumenitsa will soon have a new owner and Kavala a new terminal operator. Not surprisingly, in the first stages of the process, third parties expressed solicited interest in developing container port activities in all these ports. Adding a third operator – while avoiding monopolies – would provide users with more options and consequently enhance the competitiveness of the Greek port system.

*******

- Thanos Pallis is Professor of Port and Maritime Economics & Policy, Department of Maritime Studies, University of Piraeus, Greece; President of the International Association of Maritime Economists (IAME). George Vaggelas is Associate Professor of Shipping and Ports, Department of Shipping, Trade and Transport, University of the Aegean. They are the authors of the biannual report on Greek ports- GREPORT 2022. The article was first published in the “Posidonia 2022” special edition of the Greek newspaper “TO BHMA”.