By Theo Notteboom

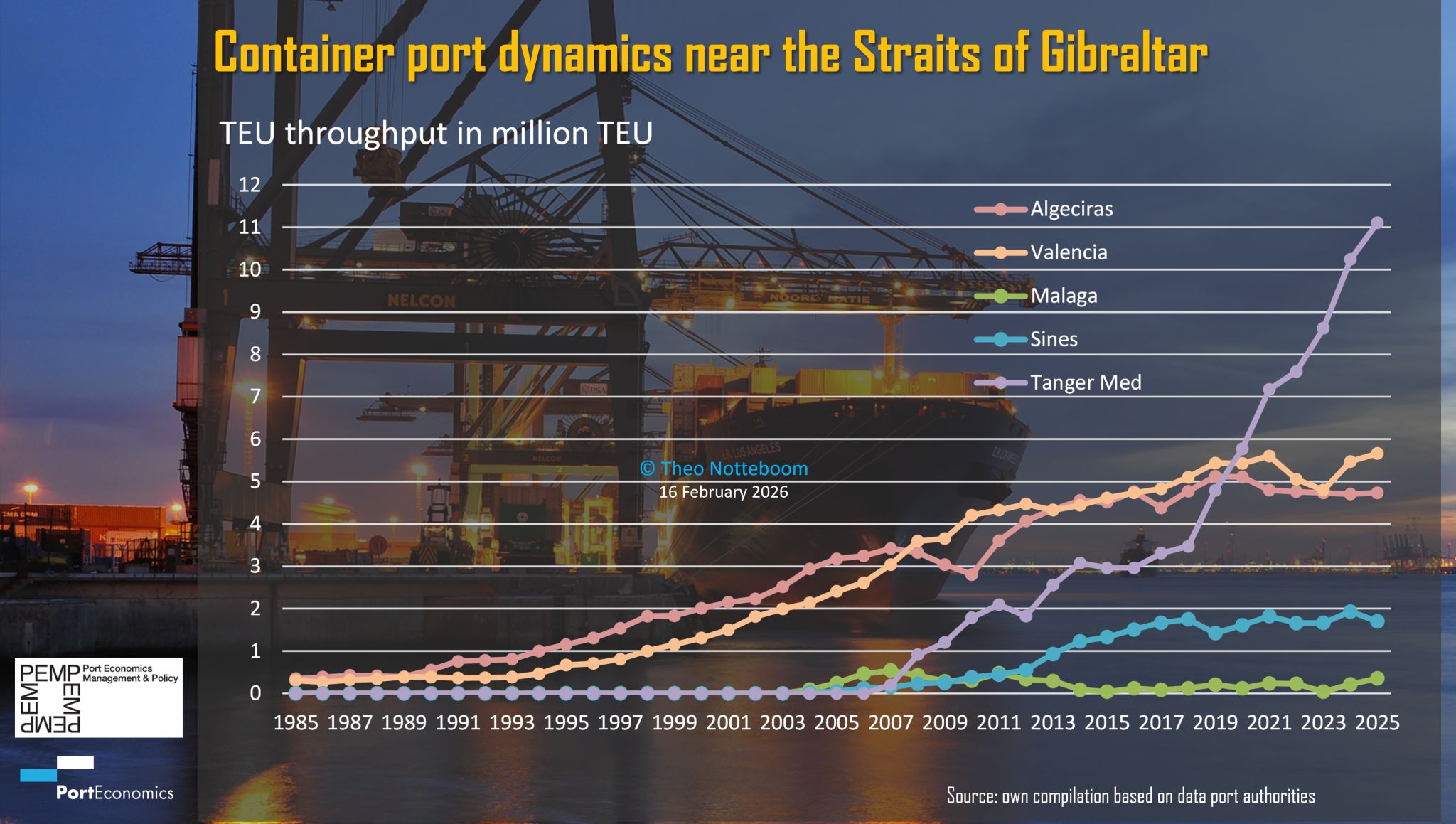

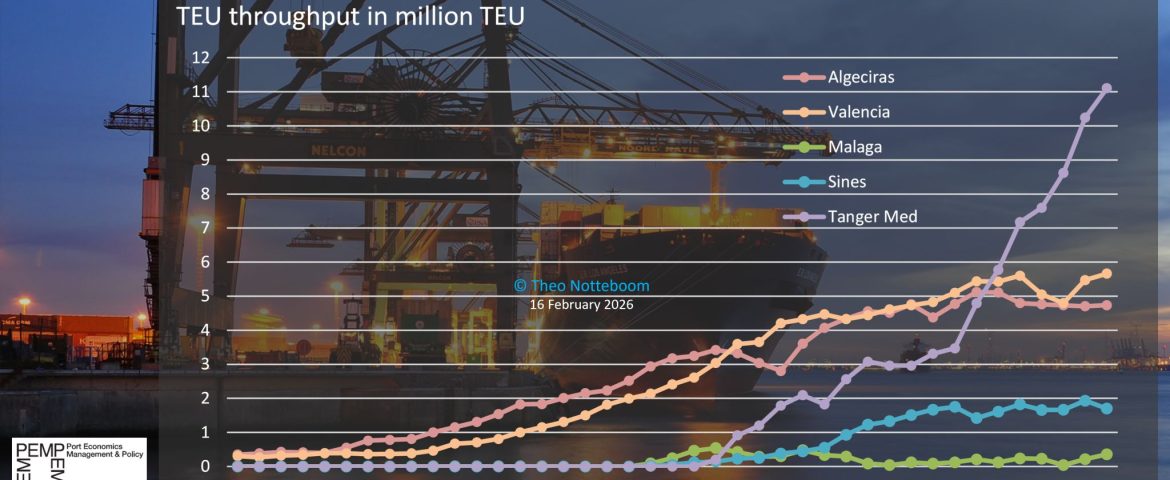

The Strait of Gibraltar occupies a pivotal position along some of the world’s most important East–West trade lanes. For many years, Algeciras, strategically located at the southern tip of the Iberian Peninsula, was the first port to fully exploit this geographical advantage by developing a transhipment hub position. In the mid‑1990s, its strong transhipment orientation enabled it to capture nearly 70% of the total container volume handled by the five ports shown in the graph. Last year, its share had fallen to just above 20%, with throughput remaining relatively stable over the past five years following the 2020 peak. Valencia, originally a gateway port, gradually expanded its presence in the transhipment market.

Sines in Portugal represents a more recent entrant in the regional transhipment arena. Sines’ share rose from 0% in 2005 to 11.7% in 2017, before gradually declining to 7.2% in 2025.

Tanger Med, which opened its first terminals in 2007, has experienced remarkable growth as successive terminals came online. By 2020, its container throughput had already surpassed that of Valencia and Algeciras. Last year, its volume exceeded 11.1 million TEU. Today, Tanger Med dominates the port system around the Strait of Gibraltar, accounting for over 47% of the total container traffic handled by the five ports included in the graph.

The rapid rise of a major non‑EU hub in close proximity to the EU port system has inevitably raised some concerns in the EU. In its January 2026 newsletter, FEPORT emphasized the vital role of transhipment ports for the EU economy and the importance of retaining such hubs within the EU. They also warned of potential traffic diversion toward non‑EU ports, a concern also echoed by ESPO (European Sea Ports Organisation), which is organizing a Brussels event on February 20 focused on the findings from the EU ETS Observatory developed by Puertos del Estado.

At the heart of this debate lies the potential impact of the recent inclusion of shipping in the EU Emissions Trading System (ETS) on EU ports, particularly regarding routing choices, hub selection, and the risk of evasive calls to neighbouring non-EU ports. The container transhipment market is highly competitive, shaped by the footloose behaviour of shipping lines. If any distortion in the level playing field would be proven, it must be addressed, as it can have immediate and visible consequences for the distribution of cargo flows among transhipment ports.