By Jean-Paul Rodrigue

Why Transshipment?

Ideally, a passenger wishing to fly from one city to another would prefer to have a direct flight. However, this is not commonly the case unless one is using the largest airports in the world such as London, Paris. New York, Hong Kong or Dubai. Even from these airports, direct flights to a wide range of destinations would not be available. The most common reason is that there is not enough volume to justify a direct service with some level of frequency. Therefore, to cope with these constraints air transportation systems tend to be organized as hub and spoke networks with larger planes servicing the hubs and regional planes connecting the smaller airports. This reflects a compromise between transport demand with customers seeking the most extensive services possible, and transport supply, where airlines are looking at the best utilization of their assets (full flights).

This example derived from air transportation can also be applied to maritime shipping. Transshipment was initially developed to service smaller ports unable to accommodate large containerships, which is commonly because of limited draft and port infrastructure. However, as maritime networks became increasingly complex, specialized transshipment hubs emerged. Unlike air transportation, transshipment requires significant yard space since containers are stored up for to a few days while waiting for the connecting ship(s) to be serviced. The growth in global trade has involved greater quantities of containers in circulation, which incited maritime shipping companies to rely more on transshipment hubs to connect different regions of the world. In 2012 the share of transshipment reached 28% of all the TEUs handled by ports around to world, double of what it was 20 years earlier.

Forms of Transshipment

Even if all transshipments are the same from an operational standpoint, moving containers from one ship to another using a port as a temporary buffer, they take place in three main forms servicing a different purpose. The first form is hub-and-spoke transshipment, which connects short distance feeder lines (and ports) with long distance deep-sea lines, linking regional and global shipping networks. The transshipment hub is usually a central location commanding access to a region. Ship capacity differs significantly between deep sea and feeder services. While the former usually involve the largest ships technically possible, feeder vessels are usually much smaller.

The second form is called intersection transshipment, where the transshipment hub acts as a point of interchange between several long distance shipping routes. It usually involve the movement of cargo between large ships since deep sea routes are prone to economies of scale. The third forms involves relay transshipment where the transshipment hub connects shipping routes along the same region, but servicing different port calls. Ship capacity can differ since regional routes can be serviced by smaller ships. Hub-and-spoke transshipment account for the great majority of transshipments (around 85%) while intersection and relay transshipment account for the remaining 15% of all transshipments.

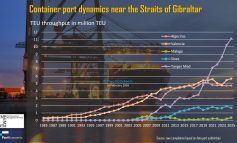

Transshipment Hubs

Geography plays an important role in the setting of a transshipment market, which is often at the crossroads of shipping routes and where there is a bottleneck such as a strait of a canal. A look at the map below underlines that they are dominantly located along the main circum-equatorial maritime route that goes through Panama, the Strait of Malacca, Suez and Gibraltar. This route is particularly used for the Asia–Middle East–Europe trade. Major transshipment hubs usually have a low maritime deviation (distance from main shipping lanes) and many provide connectivity (intersection) between north-south and east-west shipping lanes.

The degree of transshipment activity of a port can be measured by their transshipment incidence, which is the share of the total port throughput that is “ship to ship” compared with the total throughput that includes hinterland traffic as well. The higher it is, the more a port can be considered as a transshipment hub. For ports with low transshipment incidence (less than 25%), transshipment is an incidental activity, while ports having a transshipment incidence above 75% can be considered as “pure” transshipment hubs (particularly if their transshipment incidence is above 90%). On the map below the world’s most important pure transshipment hubs are shown in red.

There are seven major transshipment markets accounting for the bulk of the global transshipment activity. They are referred as markets since transshipment is an activity that is not necessarily tied to a specific port, unlike gateway traffic linked with a hinterland and inland freight distribution. Therefore, transshipment hubs compete for the traffic related to a region / market. Transshipment allows ports that would otherwise have limited maritime services because of their small hinterland to have a high connectivity to global maritime trade. This connectivity can be leveraged with the setting of logistics zones generating added value and anchoring the port’s cargo base.

![]()

The Future of Transshipment

In recent years, global transshipment incidence has stabilized in the 28-30% range, implying that transshipment is now a mature activity. Future growth is thus likely to be in proportion to the growth of global container traffic, but which factors could further increase the scale of transshipment? One important issue relates to the ongoing introduction of larger containerships calling less ports, which is inciting a greater reliance on transshipment. Further, the expansion of the Panama Canal will favor the setting of circum-equatorial deep sea services with north/ south connections, increasing the dependence on transshipment. This may be counterbalanced by port growth in developing economies such as in Latin America and Africa, which could incite more direct services with Asian, European and North American ports. Still, it remains likely that with further economies of scale and rationalization in maritime shipping (focus on selected deep sea routes) that the global transshipment incidence could reach 35%.

Because of geographical considerations, transshipment markets are unlikely to change, but which ports are the dominant transshipment hubs of these market could. The transshipment region could be stable in its level of transshipment activity while its individual transshipment hubs could experience fluctuations in their market share. The usage of transshipment hubs remains a decision made by maritime shipping companies that do so to organize their shipping networks. Such decisions can change if a company revises the allocation of its assets and its commercial strategy.

For more information: