by Theo Notteboom

by Theo Notteboom

The Straits of Gibraltar is strategically located on some of the most important East-West trade lanes. Ports in the wider region around the Straits have good reasons to convince shipping lines of making a call at their container terminal facilities for transhipment and interlining purposes.

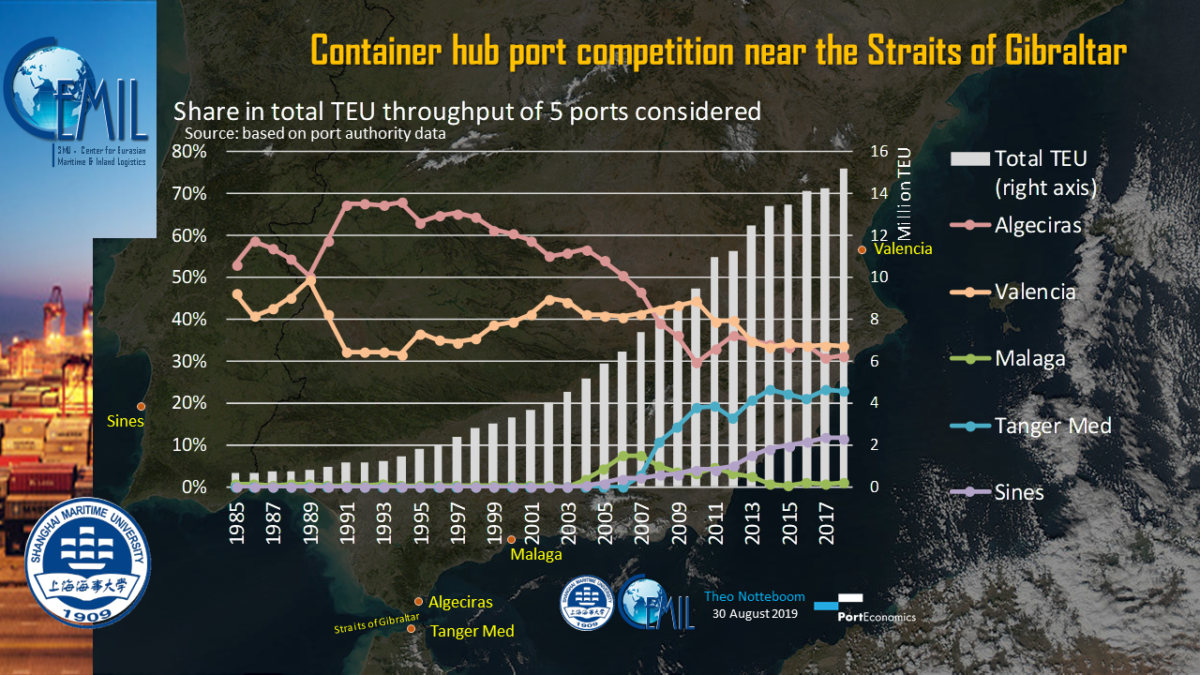

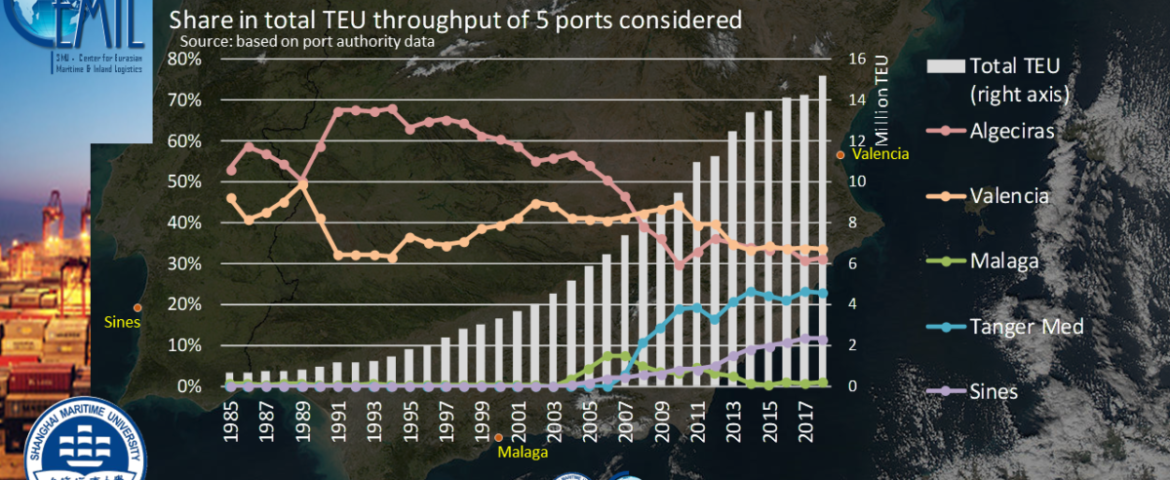

Algericas at the southern tip of the Iberian Peninsula was the first to reap the benefits of its geographical location. Its share in the total volume handled by the five ports considered in the graph reached close to 70% in the mid-1990s, but this share gradually dropped to some 35% in the 2014-2016 period and 30-31% in the past two years.

Valencia initially developed as a gateway port, but later developed a keen interest in the transhipment business as well, mainly as a result of the activities of MSC. Handling 5.1 million TEU, Valencia was the largest Med port in 2018 combining an important gateway function with significant transhipment flows. In the early 2000s, Malaga started to draw attention as a potential transhipment location. The port managed to boost volumes to about 542,000 TEU in 2007, but throughput fell to reach some 43,000 TEU in 2015. By 2018 volumes were up again reaching a modest 125,000 TEU. Growth in the first half of 2019 reached an impressive 181%, mainly driven by transit flows. The much larger hubs of Valencia and Algeciras also recorded healthy growth in the first half of 2019 (+8.7% and +8.2% respectively).

Sines in Portugal and Tanger Med in Morocco are the newest kids on the transhipment business block. Sines managed to significantly increase its share from 2.7% in 2008 to 11.7% in 2017 and 11.5% in 2018. MSC has a strong presence in Sines, a port which is particularly keen on developing a turntable position in the trade between Asia, Europe and South America. Tanger Med increased its market position in the Straits region from 10.7% in 2008 (a year after the opening of the first terminals) to 23.2% in 2017. The Moroccan port saw its market share drop to 22.8% in 2018 due to capacity constraints on its existing facilities. However, the construction works on the Tanger Med 2 which began in May 2010, will bring the total capacity of the port to about 9 million TEU. A part of Tanger Med 2 became operational earlier this year. However, other ports in the region are planning massive terminal expansions.

The largest development involves the extension of the port of Valencia adding an additional capacity of about 5 million TEU (to be operational by 2024-2025). In July 2019, the Portuguese Government approved the decree laws that establish the basis for the concession of a new container terminal in Sines, i.e. the Vasco da Gama Terminal with a planned capacity of 3 million TEU, and the expansion of the existing Terminal XXI (from 2.3 million TEU to 4,1 million TEU).

A final note: the ports near the Straits of Gibraltar are facing increased competition from other ports. For example, Barcelona is attracting more and more transhipment containers recording a growth of 35% in this market segment in 2018.