By Ricardo J Sanchez[1] & Alejandra Gomez Paz[2]

[1] Co-director, Kühne Professorial Chair in Logistics, School of Management, Universidad de los Andes, Colombia

[2] Member of the Kühne Professorial Chair in Logistics, School of Management, Universidad de los Andes, Colombia

Acknowledgments: special thanks to Christoph Schaar for his contributions.

The difference between accessibility and connectivity is often seen as a “merely” theoretical question posed from an “academic” point of view as if downplaying its scope.

Conversely, when a purely “technical” standpoint is taken, it is argued that it reduces the issue to the organisational structure of the itineraries, dependent “only” on technical issues.

In the present article, the authors make an effort to take the discussion to a level in which both theoretical and practical factors may be properly revalued. To this end, it is essential to begin by defining the concepts, noting that they are intrinsically linked.

Accessibility is the measure of the capacity of a location to be reached from, or to be reached by different locations. Therefore, the capacity and the arrangement of transport infrastructure are key elements in the determination of accessibility (Rodrigue, 2024). Geographic accessibility, via shipping liner services or any other means of transport including air, is closely linked to the configuration of the regular networks provided by carriers. At the same time, that configuration is defined by the service demand (from the “no cargo, no service” condition).

Connectivity, as another quantitative measure, defines the quality’s condition of the accessibility, involving rates, reliability and other economic and operating constraints.

Basically, if a cargo can be carried from any point in the Caribbean to any location worldwide, including regional and national destinations, there is not an issue with accessibility. However, if this accessibility is costly, unreliable, or hampered by a lack of genuine competition, then a significant problem with connectivity arises.

In brief, connectivity is a broader conception than accessibility, and it is the result of the interaction between economic, technical, market and operating issues.

This brief study places special emphasis on accessibility while cautioning that it is necessary to promote in-depth studies on connectivity. It contributes the implementation of data-science tools to achieve a better treatment of accessibility in the Caribbean, as a step towards a necessary study on the measurement of connectivity, which is the main problem in the Caribbean. The rationale behind this is based on direct empirical evidence from Caribbean countries and territories (even in small samples), where it is possible to observe that consumer goods, including durable goods, are priced significantly higher than in their countries of origin, and that this can be attributed to connectivity problems, among others, even when accessibility is similar.

Connectivity, as a quality’s condition of any country’s accessibility and integration within the transportation network, has a direct impact on trade among countries and regions, and consequently on their economic development. Research by Hoffmann (2019), Fugazza and Hoffmann (2017), Shepherd (2017), Wilmsmeier (2014), Hoffmann and Wilmsmeier (2008), Hoffmann, Sanchez and Wilmsmeier (2006), among others, underscore the fact that enhancing maritime connectivity can significantly drive down costs and positively influence trade outcomes and development.

The primary objective at hand is to gauge accessibility by examining the interconnections within the maritime transportation network facilitated by liner services between ports, countries, and regions. This is an initial step towards understanding network dynamics and aiding decision-making processes. Specifically, the study delves into the behaviour of liner service offerings per connection route and the involvement of carriers in the Greater Caribbean – from the USA Gulf to the North Coast of South America, and the Caribbean islands. The findings stem from a “Liner Services Matrix” crafted through Data-Driven Science Techniques, complemented by the continually updated Liner Shipping Connectivity Index (LSCI) maintained by UN Trade and Development (ex UNCTAD), which refers to direct accessibility among countries (LSCI or LSBCI), or ports (PLSCI).

However, it is necessary to acknowledge that connectivity between country pairs is influenced by factors beyond the configuration of liner services and their operators. This includes maritime freight rates, trade volumes, port infrastructure, and operational practices. Gomez Paz A. and Sánchez R. J. (2021) outline critical barriers affecting bi-regional trade and emphasize the need for policy interventions to mitigate them. These barriers encompass hinterland transportation networks, business practices related to service reliability, and the formulation of long-term policies.

In evaluating accessibility, the study delineates several parameters intrinsic to the liner shipping network:

“Geographical coverage,” signified by the ports of call in the itineraries, enabling direct connections -links- between various country pairs across diverse regions, thereby offering multiple transport options by transshipment. Also called network reach.

“Weekly capacity,” reflecting the available slot space at each port along the service route -allocation- measured in Twenty-foot Equivalent Units (TEU). This metric is closely linked to the dimensions of vessels deployed within the services, which impact port infrastructure configurations and associated logistics services.

“Carriers participation” significantly influences the array of available maritime transport and logistics service alternatives.

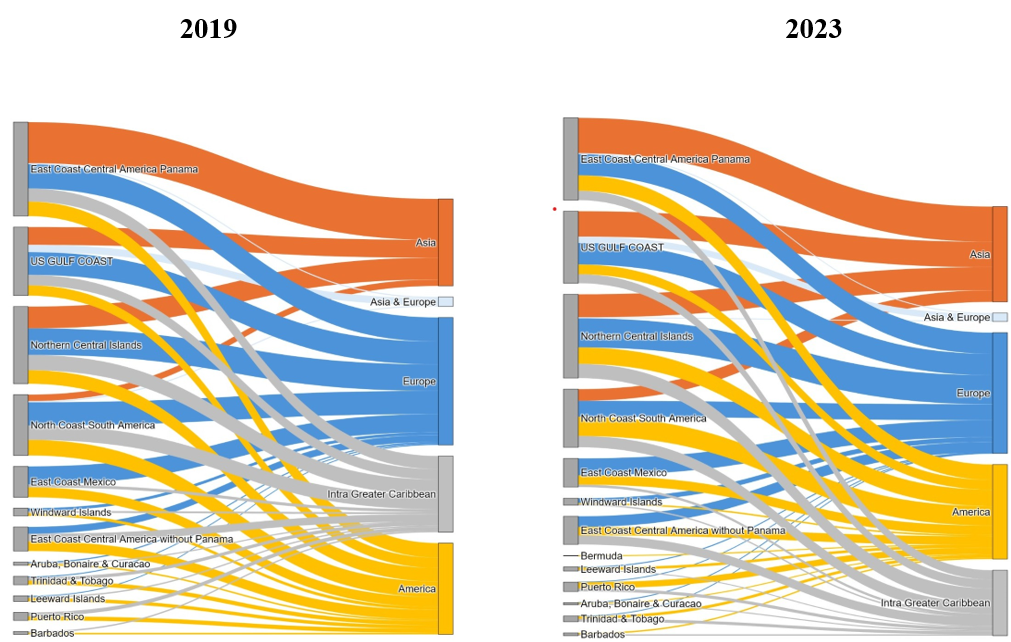

Caribbean accessibility, geographical coverage between 2019 and 2023

As can be observed from Figure 1:

- Greater Caribbean regions have substantial liner shipping flows across the Atlantic and the Pacific to Europe and Asia, showing their strategic importance in global trade.

- Although Asia and Europe are primary geographical coverage, measured by weekly nominal capacity, there’s a significant spread across various regions, indicating a diverse global trade network.

- There are significant flows from the East Coast Central America Panama to Asia and Europe, indicating this is the region with major geographical coverage. Flows from regions such as Northern Central Islands and US Gulf Coast also prominently connect to Asia and Europe, followed by North Coast of South America.

- The pattern flow is consistent between 2019 and 2023. The comparison reveals a significant increase in specific key routes to Asia, particularly those from the US Gulf Coast and North Coast South America to Asia, 62% and 107 %, respectively. Meanwhile, flows from East Coast Central America Panama to Asia have remained relatively stable, underscoring their continued importance in global trade. The port of Cartagena stands out on the North Coast of South America.

Figure 1: Weekly nominal capacity by geographical coverage -direct link between region within Greater Caribbean and global regions around the world – 2019 vs. 2023.

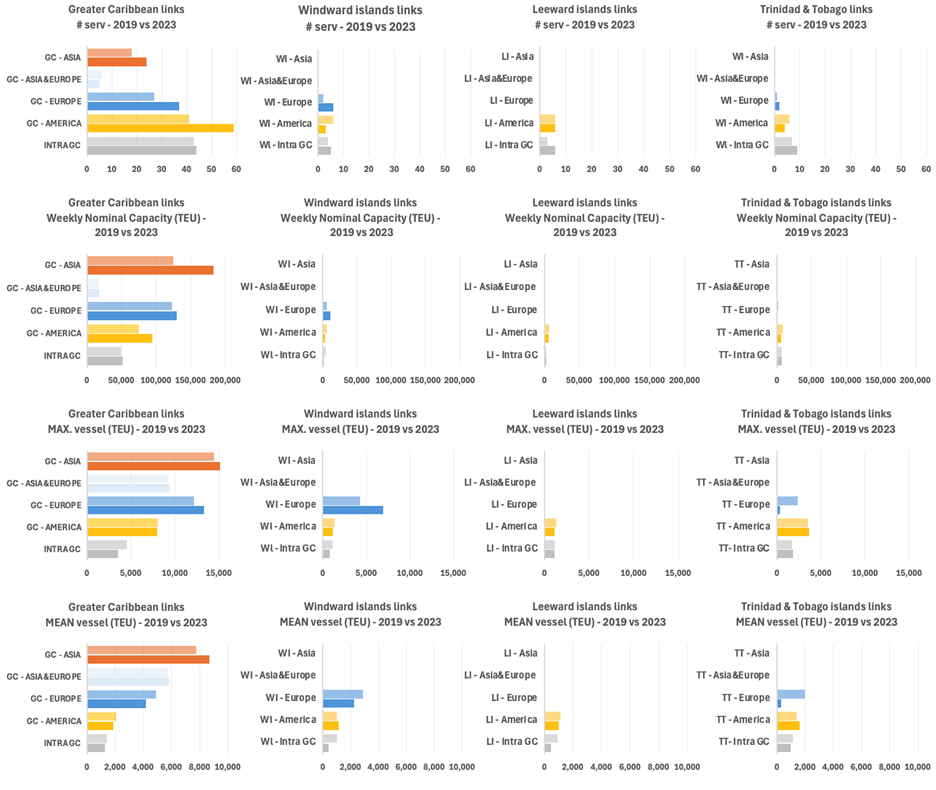

Accessibility evolution between 2019 and 2023

Figure 2 (from a to p) allows to observe that:

- Across all regions, there’s a notable increase in the weekly nominal capacity linking Greater Caribbean with Asia and Europe, as shown in Fig 1. This is reflected in the number of services and the maximum and medium vessel size variables as well.

- The largest ship deployed in the Greater Caribbean services for the routes to Asia reached a commercial capacity of 15000 TEU in 2023. This is larger than the largest ship in 2017 with 13200 TEU. The cascading phenomenon is also evident in the routes to Europe. In 2023, the largest ships reached 13300 TEU, and in 2017, they reached 10500 TEU.

- The Intra Greater Caribbean routes show increased services and weekly nominal capacity, strengthening regional connectivity. However, the maximum and mean vessel size slightly decreased. The vessel sizes deployed in the Intra Greater Caribbean routes range from 120 TEU to 1900 TEU.

- Between the Caribbean islands, the Northern Central Island region present largest weekly nominal capacity and extended geographical coverage to Asia and Europe. On the contrary, the islands grouped as Windward Islands and Leeward Islands and Trinidad & Tobago present less weekly nominal capacity and limited geographical coverage to America and in Intra Greater Caribbean. Also, negligible coverage from Windward Islands and Trinidad & Tobago to Europe is identified.

Figure 2: Number of services; Weekly nominal capacity, MAX and MEAN vessel size, 2019 vs 2023.

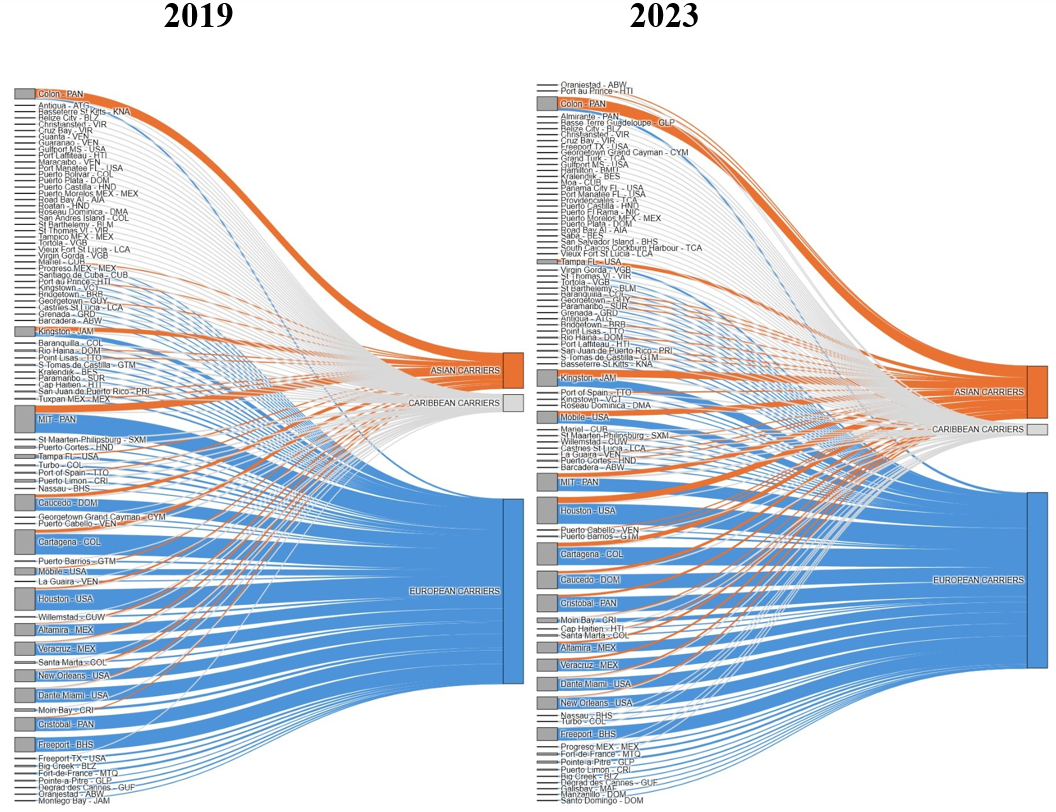

Players in the Caribbean islands

As can be observed from Figure 3:

- Greater Caribbean ports are served by carriers based in Europe, Asia, and locally, illustrating a diverse and interconnected regional network. In general, the European carriers serve all global regions, the Asian carriers are mostly present in links to Asia, and local carriers cover intraregional services.

- European carriers are the main operators in the Greater Caribbean market (measured by nominal capacity), with a sustained participation from 2019 to 2023. One observed behaviour is the acquisition of feeder carriers. For instance, American carrier APL acquired by CMA-CGM in 2016.

- Even though Asian carriers have less market share, they increased participation measured in number of port calls by a 50% and in nominal capacity by 25% CAGR in the period 2019-2023. Notably, the Asian feeder carrier X-Press is present in the intra Greater Caribbean link.

- Ports such as MIT, Cristobal and Colon in Panama appear as major hubs with numerous liner services offered by different carriers. Hub ports in the US Golf, such as Houston, and Miami in the Atlantic; strategic locations such as Freeport, Bahamas; Caucedo, Dominican Republic; Kingston, Jamaica and Cartagena, Colombia are served by multiple carriers from different origins.

Figure 3: European, Asian and Regional carriers’ participation by main ports in the Greater Caribbean, 2019-2023.

Notes to figures:

Figure 1: Weekly nominal capacity by geographical coverage -direct link between region within Greater Caribbean and global regions around the world – 2019 vs. 2021.

This Sankey diagram visualizes accessibility by examining the liner services offered in the Greater Caribbean, which have direct link connections to all regions around the world.

Left side nodes: Regions within the Greater Caribbean. Each region groups the ports geographically located nearby – go to Figure 4 to see the ports and their region by a map visualization.

Right side nodes: Global regions. Each region groups ports that share a global pattern destination. Asia; Asia& Europe; Europe; America without Greater Caribbean; and Intra Greater Caribbean. Itineraries grouped in the link Greater Caribbean–Asia include ports in the Greater Caribbean and ports in Asia, Africa, India and Oceania, from America’s point of view. Asia & Europe refers to itineraries that include ports in the Greater Caribbean, Asia and Europe (generally the services that go around the world). Europe relates to the itineraries with calls in the Greater Caribbean and Europe included the Mediterranean ports and the port in the Strait of Gibraltar. America concerns itineraries with ports in the Greater Caribbean and East and West Coast in America. Greater Caribbean apply to itineraries with call exclusively in the Greater Caribbean.

Flow: The lines between the left and right sides represent the link (from-to), illustrating the geographical coverage of the ports grouped by Greater Caribbean regions. The width of each line reflects the Weekly nominal capacity of the liner services configuring the link from-to. Wider lines indicate higher capacity, so higher accessibility. Weekly nominal capacity by port by link refers to the sum of the mean capacity of the services that call the port and have the same geographical coverage; Weekly nominal capacity by region by link refers to the sum of the mean capacity of the services that call the port inside a region and have the same geographical coverage (data assumption: all services with weekly frequency)

Colour Coding: Different colours differentiate the scope.

Please note the regional comparison and evolution:

(i) Changes over time: see how the flows -links capacity- worth, and nodes linked changed between 2019 and 2023.

(ii) Regional focus: see how the geographical coverage varies across the Windward Islands, Leeward Islands, and Trinidad & Tobago.

(iii) While this diagram focuses on direct connections, ports located in regions with less geographical coverage can extend their reach through transshipment and leverage routes that include ports with those connections to access additional global regions.

Figure 2: Number of services; Weekly nominal capacity, MAX and MEAN vessel size, 2019

The figure illustrates the evolution of main variables that characterize liner services in the Greater Caribbean and its subregions (Windward Islands, Leeward Islands, and Trinidad & Tobago) grouped by geographical coverage between 2019 and 2023. The graphs are organized into four key metrics: number of services (#), Weekly nominal capacity (TEU), maximum size, and mean size of the vessel deployed in the services (TEU).

Please note the evolution and regional comparison:

Geographical coverage: observe differences in variables (number of services, weekly capacity, vessel size) for each geographical coverage.

(i) Changes over time: see how these metrics have changed between 2019 and 2023.

(ii) Regional focus: see how these metrics vary across Windward Islands, Leeward Islands, and Trinidad & Tobago.

Next outputs, ongoing:

(i) Additional variables: frequency (days), calls (#), duration (days), minimums size of vessels (TEU), vessels (#), Nominal Capacity, carriers’ participation by Vessel Slot Agreements (#).

(ii) Regions: East and West Coast of South America.

Figure 3: European, Asian and Regional carriers’ participation by main ports in the Greater Caribbean, 2019-2023.

This Sankey diagram effectively maps out how different ports are served by vessels deployed by European, Asian,

Caribbean and American, and other carriers.

Left side nodes: Ports in the Greater Caribbean. Port´s name- Country code ISO3.

Right side nodes: Carriers that offer the liner shipping service by Vessel Sharing Agreements.

Flow: The lines between the left and right sides represent the relationship between the port and those who offered services at those ports. The width of each line reflects the sum of the Nominal capacity of the liner services group by their origin -European, Asian, Caribbean and American. Wider lines indicate higher Nominal capacity, so higher carrier market penetration. Nominal capacity by port by carrier refers to the sum of the vessel’s capacity deployed by carriers on the services that call the port.

Colour Coding: Different colours differentiate the carrier’s origin.

European carriers: MSC; CMA-CG; APL; MAERSK-LINE; HAMBURG-SUD; SEA-LAND;

HAPAG-LLOYD; MARFRET, GEEST

LINE; SAFMARINE; STINNES; STREEMLINES.

Asian carriers: EVERGREEN LINE; ZIM; COSCO; OOCL; HYUNDAI; ONE; WAN-HAI; X-PRESS; YANG-MING; GAL-GULF; MOL; NYK.

Caribbean and American Carriers: SEABOARD-MARINE; CARIBBEAN FEEDER; CROWLEY; DOLE; KING OCEAN; TROPICAL SHIPING; TOTE-MARINE; GREAT-WHITE; NIRINT; SEATRADE; HYDE-SHIPPING-CORP; LINEA-PENINSULAR; MELFI-MARINE; NATIONAL-SHIPPING-OF-AMERICA; SEACAT-LINE; SOMER-ISLES; SOREIDOM; WORLD-DIRECT-SERVICE; BERMUDA-CONTAINER-LINE.

These carriers served the Greater Caribbean between 2017 and 2023.

Please note the evolution and regional comparison:

(i) Changes over time: see how the flows width and nodes linked -carriers participation or market penetration- changed between 2019 and 2023.

(ii) Port focus: see how the carriers participate across the ports in the Greater Caribbean

Final observation: Dear reader, please feel welcome to challenge the data! Should you observe any inaccuracies, we would appreciate if you could notify it to us.