By Theo Notteboom

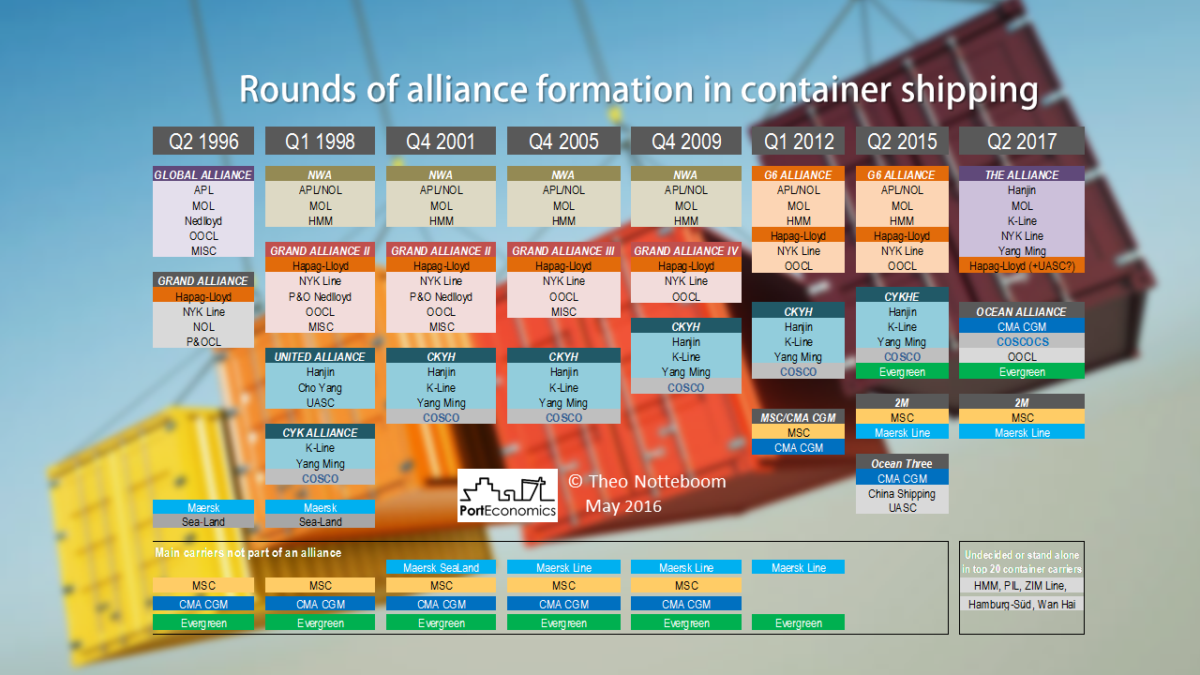

Alliances are about operational vessel-sharing co-operation between container shipping companies on multiple trade routes (mostly east-west). The first strategic alliances between shipping lines date back to the mid-1990s, a period that coincided with the introduction of the first post-Panamax containers vessels on the Europe-Far East trade. The alliance partnerships evolved as a result of mergers and acquisitions (e.g. merger between P&OCL and Nedlloyd and the take-overs by P&O Nedlloyd and SeaLand by Maersk) and the market entry and exit of liner shipping companies.

Today, four alliances are operational in the market: 2M, Ocean Three, CKYHE and G6. However, the recent merger of China Shipping and Cosco to form China Cosco Container Lines (COSCOCS) and the acquisition of APL/NOL by CMA CGM already signalled upcoming major changes in the current alliance structure. The new alliance landscape has become more clear in the past weeks. The 2M alliance will remain. Subject to regulatory approval, two new large-scale alliances will start operations in Q2 of 2017: Ocean Alliance and THE Alliance. There are still a few unknown factors though. First, Hapag-Lloyd and UASC are still in talks about far-reaching cooperation or even merger, so UASC might end up being part of THE Alliance. Second, Hyundai Merchant Marine (HMM) is a remarkable absentee in the latest round of alliance formation. Third, it remains to be seen whether some of the other top 20 carriers might eventually go for alliances (think of ZIM Line or Hamburg-Sued) or will rely more on ad hoc vessel-sharing agreements (VSA).

Despite the announced changes, it is dangerous to conclude that the dance of the alliances will be finally over in Q2 of 2017. The graph clearly shows that strategic alliances have seen many changes in the past. Individual shipping lines continue to show a high level of pragmatism when setting up partnerships with other carriers. There seems to be no such thing as a fixed dancing partner.