By Theo Notteboom

The global container shipping fleet has experienced significant growth over the past few decades, driven by the steady rise in international trade. Shipping lines have expanded their fleets either through organic growth—as in the case of MSC—or through a combination of organic growth and mergers & acquisitions, like Maersk.

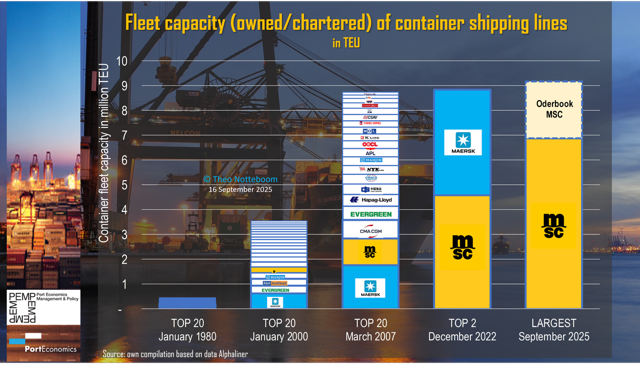

Today, the top 20 container carriers collectively operate a fleet (including both owned and chartered vessels) with a total capacity of 30 million TEU. Three years ago, this figure amounted to 24 million TEU. It was 8.7 million TEU in 2007 and 3.5 million TEU in 2000. In 1980, the total fleet capacity of the top 20 carriers was around 435,000 TEU. To put this in perspective, Pacific International Line (PIL)—currently ranked 11th among container carriers—operates a fleet of roughly the same size today.

By late 2022, the combined fleet capacity of the top two – MSC and Maersk – had already exceeded the total capacity of the top 20 carriers back in 2007. MSC’s current fleet is now less than 2 million TEU shy of the entire top 20 fleet capacity in 2007. Furthermore, its capacity is almost double that of the top 20 carriers a quarter-century ago. MSC also has an orderbook of 2.3 million TEU, signaling continued expansion.

Read all about the container shipping market in the updated chapter of our online textbook ‘Port Economics, Management and Policy’ – PEMP (Theo Notteboom, Thanos Pallis and Jean-Paul Rodrigue) here.

We are currently finalising the manuscript for the second edition of the book, which incorporates substantial new material. Stay tuned!