By Jean-Paul Rodrigue

For many years, the shipping industry has been in a situation of overcapacity, which was depressing rates and impairing the profitability of shipping lines. To make matters worse, almost every major shipping line was ordering larger containerships, caught in a vicious circle of trying to boost profitability with economies of scale. Capacity was growing faster than demand. In such as setting, there were discussion and rumors within the industry about which major shipping company would fold first in an environment that underlines limited future growth prospects and zero-sum game competition. In September 2016, the Korean company Hanjin Shipping filed for bankruptcy, which represents the largest bankruptcy in the shipping industry in recent years.

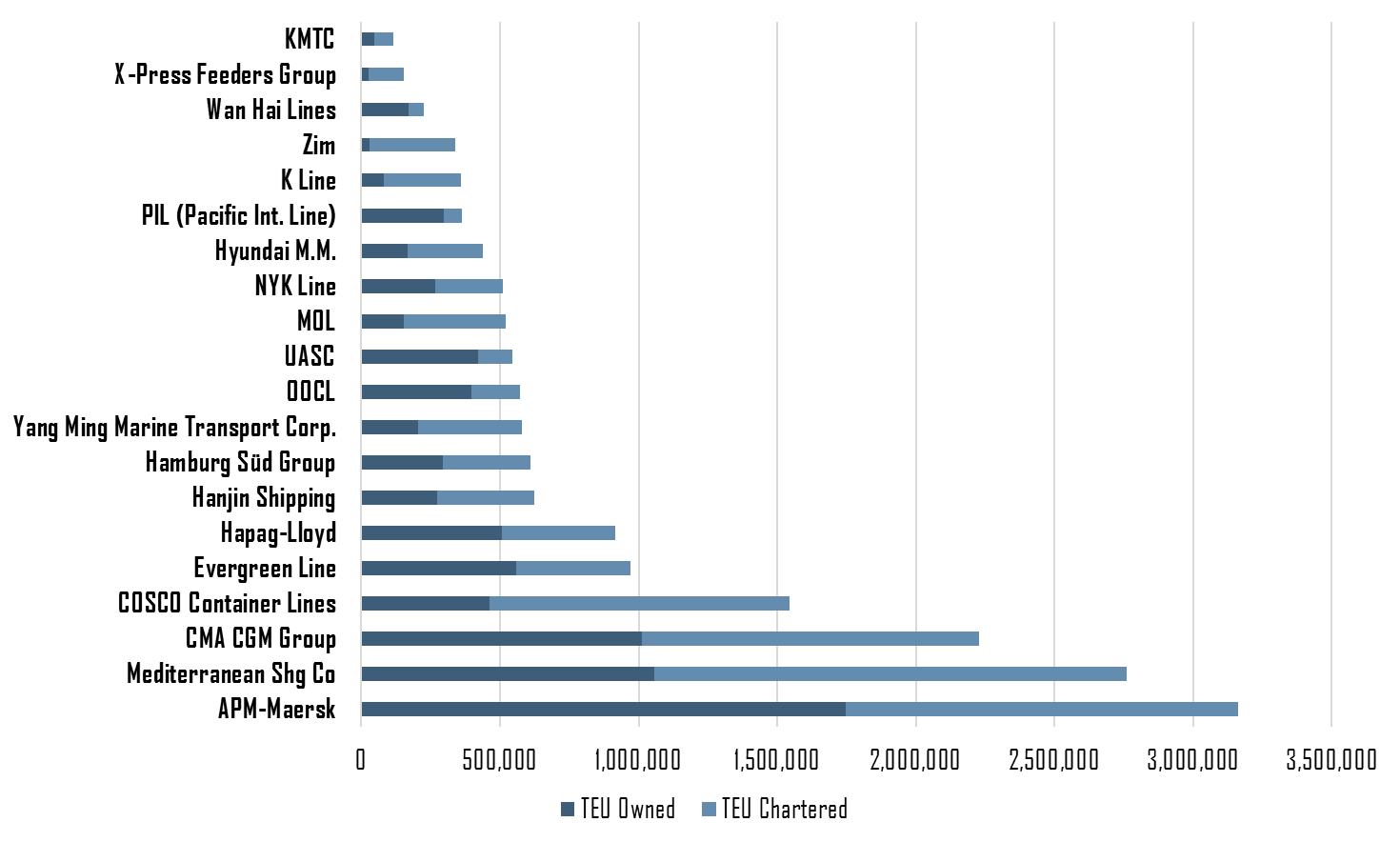

As of September 2016, Alphaliner reports that Hanjin owned 37 containerships and chartered 62 others, making it the world’s seventh largest container shipping line, which represents about 3.2% of the global container shipping capacity (Figure 1).

Figure 1: Containership Capacity of the World’s 20 Largest Shipping Lines, September 2016. Source: Alphaliner.

Even if this share is relatively small, this is still more than 623,000 TEU of shipping capacity that has been disrupted. Further, a large share of this capacity is allocated on transpacific routes as well as routes from Asia to Europe. Although Hanjin is a global shipping line, it has a pronounced regionalism.

The 37 containerships directly owned by Hanjin are subject to the full asset seizure by creditors under bankruptcy protection, but the matter is more complex for the 62 chartered ships. In theory, chartered ships fully belong to the leasing company and are thus not subject to seizure, only to be declined services since a terminal operator may not get paid by the company under receivership. This is a risk that many are unwilling to assume. However, many chartering agreements are under “bareboat” conditions where the owner gives possession of a containership to the shipping line, who assumes all the operational costs, including crew, fuel, insurance and terminal charges. Such chartering arrangements can be used as a form of ship financing, which could lead to legal complications in terms of if the ship was truly leased or if the chartering arrangement is a sale in disguise.

Hanjin is also a terminal operator with substantial stakes and leasing agreements (Table 1).

Table 1: Container Terminals where Hanjin has a Stake (as of 2015) (Source: Adapted from Drewry Shipping Consultants)

Hainjin has stakes in 20 container terminals, totaling and annual capacity of 22.4 million TEU. Looking at this portfolio, it is clear that Korea has the most significant potential terminal capacity disruptions, including Busan which is an important transshipment hub for the China trade. It remains uncertain about under what conditions operations will continue in terminals where Hanjin has a majority stake, but for terminals where Hanjin has a minority stake, disruptions are unlikely since the terminal operating company is a separate entity (Hanjin being a simple shareholder). The main issue is that the majority of these terminals will lose ship calls from Hanjin, which could impair their profitability and force some to restructure.

The specific orientation of Hanjin, both in terms of trade routes and terminal assets implies a focused impact of its bankruptcy. We argue that this will impact global shipping and supply chains over three stages. The first stage involves a “shock” for supply chains that were using Hanjin, since services are interrupted without prior notice. Cargo becomes stuck in transit as shippers (ports, transport companies) are refusing to handle Hanjin ships since they would likely not get paid for that service. This is highly disruptive for supply chains because of the scale involved. The Wall Street Journal reported that about $14 billion worth of cargo was caught in transit on Hanjin ships when bankruptcy was declared. However, provisions and funds are being made available to make sure that the cargo gets unloaded and made available to be transported by other carriers. Cargo owners thus have to renegotiate the transport of their cargo with new carriers, inducing a surge in rates on routes and ports where Hanjin was providing substantial capacity. This is expected to last about one month, with the involved supply chain gradually returning to normal as the stranded cargo is reclaimed and put back on its respective supply chains. There will be some delays and shortages, but the cargo will eventually be delivered.

In the second stage, the increase in rates and the capacity demand on routes and ports that were serviced by Hanjin will incite competitors to quickly offer additional services and capture such low hanging fruits. Since the industry is in a situation of overcapacity, this will put a downward pressure on rates rather quickly as shipping lines aggressively compete to gain market share. Within three months, the shipping industry will likely have completely substituted services that were offered by Hanjin.

The last stage concerns the allocation of Hanjin’s assets. With liquidation, most of its assets will be captured at discount prices, giving opportunities to established actors and even new entrants. Although some ships could be retired, most will be brought back into service, which will continue the downward pressure on rates until a pre-bankruptcy equilibrium is reached. At that point, it is likely that the shipping industry will be in a situation as if the bankruptcy never occurred. Although the bankruptcy of Hanjin is a significant event in global container shipping, the situation of overcapacity ensures that the shock will be short lived and quickly absorbed. While competitors may rejoice, this reflects an enduring weakness of the shipping market. Who will go bankrupt next?