By Jean-Paul Rodrigue

The St. Lawrence, as a gateway to Eastern Canada, is contemplating an emerging risk in the Post Panamax context, which is undermining its commercial viability for containerized maritime shipping. The Port of Quebec handled containers in the early stages of containerization, but by the late 1970s all this traffic shifted to Montreal because of its notable market advantage and excellent connectivity to the Ontario and Midwest hinterland.

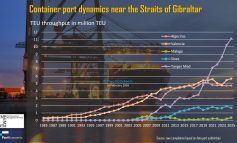

However, technical changes in containership sizes are gradually challenging this advantage, marginalizing Montreal further as a long-term commercial option. With a draft of about 11 meters the port can only handle containerships of around 2,500 TEU. Larger ships remaining below the Panamax standard (about 4,500 TEU) can also be handled if they are not fully loaded. The port, even with its Contrecœur expansion project, is unable to move beyond these technical limitations. Meanwhile, the last 20 years have seen a surge in the average ship size and the 2016 expansion of the Panama Canal has incited a paradigm shift on the eastern seaboard of North America. Conventional Panamax ships are being quickly removed from many services and replaced by larger post-Panamax ships that are more cost effective to operate. Montreal is finding itself in a weakened position.

A proposed technical fix is dredging the seaway channel between Montreal and Quebec to an anticipated depth of 12.3 meters (from its current depth of 11.3 meters), which is a highly expensive and controversial endeavor. Even if implemented, it would lead to limited technical gains since it would allow an additional 1,000-1,500 TEU of ship capacity (to around 4,000 TEU), making the port barely at the Panamax level. From a simple cost / benefit point of view, the merits of both Contrecoeur and the dredging of the seaway channel between Montreal and Quebec are doubtful.

An approach would be to leave the situation as is, keeping Montreal as a lucrative and effective niche port. However, this approach runs the risk on the medium term of undermining the competitiveness and the connectivity of Eastern Canada. In addition to the high risk of stagnation, and even gradual declines in volumes, there is also a risk that one or more shipping lines currently calling the port of Montreal may elect to cut back or even cancel their services. For instance, in the summer of 2017, the Chinese shipping giant COSCO purchased OOCL, which is regularly calling Montreal. The question remains about how COSCO after the acquisition will restructure its North American shipping network and how Montreal will fit into this new picture.

With the development of intermodal rail corridors and inland ports, the North American port hinterland is becoming increasingly competitive, undermining the market areas that many ports conventionally considered as their own. In 2015, the American rail operator CSX opened a new intermodal yard in Valleyfield, just south of Montreal. This new terminal is connected to the Eastern seaboard network (including ports such as Hampton Roads) and thus offers additional options for cargo owners in Eastern Canada. Even if this new intormodal rail terminal is just a small fraction of the capacity of the port of Montreal, it is a signal that the competitive environment is shifting.

Under this constraining context brought forward by external factors both on the maritime and inland sides, a new Post-Panamax container port facility around Quebec City is an option that merits careful consideration. The strategic objective is to ensure that Eastern Canada retains and possibly expans its container volumes through a dual port strategy taking into account these issues:

- The strategy takes place in a zero-sum game environment, meaning that a great share of the traffic that would be handled by a new deep-sea port terminal would come at the direct expense of the traffic handled at the port of Montreal. It is essentially a partial relocation of the port of Montreal so that it can be accessible to the Post-Panamax shipping market. Although this is unfortunate, it is necessary as a long-term strategy to remove the technical constraint of limited draft out of the commercial decisions of shipping lines to call a port.

- The project involves a duplication of port infrastructure that at the first glance appears counter intuitive since the volumes handled by the port of Montreal have shown almost no growth over the last 10 years. The port handled 1.44M TEU in 2016 while it handled 1.47M TEU in 2008. This duplication is necessary because of the strategic importance of enabling post-Panamax container ships to service the Quebec-Ontario corridor. Still, there may be new niche opportunities that the post-Panamax project could expand and serve, but these on their own are not sufficient to justify the project.

- This strategy requires the St. Lawrence to be considered as a port cluster. Since Montreal has been for decades the single container port along the St. Lawrence, its vision is constraining future developments since its sole options are to stay with its business case and invest in infrastructure within its jurisdiction (e.g. Contrecoeur project). Collaboration with the Port of Montreal is essential to ensure an effective transition to a dual Montreal-Quebec port strategy. This could take several forms, including a merger of the Port Authorities or simply a joint venture involving the terminal project. The goal is not to compete with Montreal, but to upgrade the port cluster to a Post-Panamax setting and therefore expand the commercial potential of Eastern Canada.

In light of this new strategy, the Port of Montreal would need to seriously reconsider its infrastructure development options to include Quebec (or the St. Lawrence). The current context forces a consideration of options going beyond limiting jurisdictional constraints. Both the status quo and the new strategy come with risks, but the outcome of the status quo most likely leads on the medium term to a declining importance of the St. Lawrence in container shipping.

It is ultimately to the market to decide the potential respective share of Montreal and Quebec in the St. Lawrence port cluster. The current lack of options may incite supply chain managers to consider other alternatives on the East and West coasts.