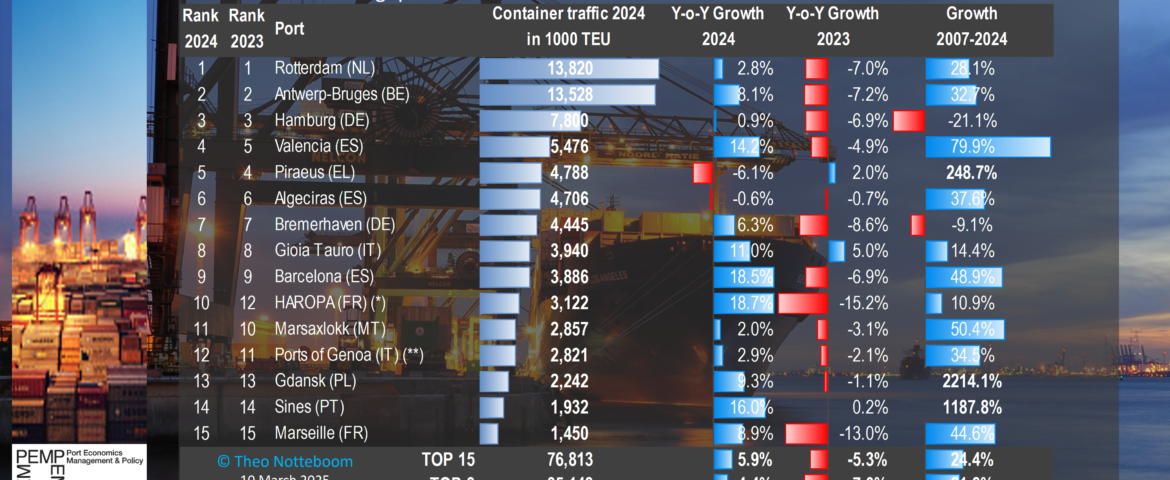

The 2024 ranking of the top 15 EU container ports highlights both stability on the top of the ranking and significant changes in port performance for the remaining ports. Rotterdam retains its position as Europe’s largest container port, handling 13.82 million TEUs, followed closely by Antwerp-Bruges at 13.53 million TEUs. Hamburg remains in third place with 7.8 million TEUs, while Valencia moves up to fourth place, benefiting from strong 14.2% growth.

Following, the graphic below presents the ranking of the top 15 EU container ports in 2024, providing insights into their year-on-year growth and long-term trends.

Keynotes and shifts:

- Rotterdam and Antwerp-Bruges continue to lead, with only a narrow difference in throughput.

- Valencia moves up to fourth place with a 14.2% growth.

- Gioia Tauro (+11.0%) and Gdansk (+9.3%) saw significant increases in container trhroughput.

- Piraeus (-7.8%) and Sines (-13.0%) experienced declines, affecting their rankings.

- The total throughput of the top 15 EU ports reached 76.77 million TEUs, a 5.9% year-on-year increase, despite variations in individual port performance.

PortEconomcis member Theo Notteboom, has compiled the database and analyses the data:

“The top 15 EU ports combined handled 76.8 million TEU in 2024 or 5.9% more than in 2023. While 2023 was characterized by a strong to moderate traffic decline in most ports, 2024 brought double-digit growth in five of the top 15 ports, with another four ports recording a volume increase between 5 and 10%.

The container throughput of the top 3 EU ports increased by 4.4% in 2024 after it tumbled around 7% in 2023. Among the top three ports, the Belgian port of Antwerp-Bruges shows the best performance by far with 8.1% y-o-y growth, almost triple the growth of nearby Rotterdam. As a result, the TEU gap between these Benelux ports has become razor-thin (see my earlier Linkedin post). Hamburg’s volume stagnated.

Bremerhaven saw a healthy traffic development (note that the growth rate relates to the first 11 months of 2024). Other top 15 EU ports of the Le Havre-Gdansk range include HAROPA and Gdansk. They even outperformed Antwerp-Bruges and Bremerhaven, realizing +18.7% and +9.3%, respectively. In doing so, HAROPA more than compensated for its traffic losses incurred in 2023, while Gdansk continues its growth path despite ongoing terminal extension works at the Baltic Hub.

The impact of the Red Sea crisis and the associated shipping network modifications are traceable in the Greek port of Piraeus which is the only port facing significant traffic losses (minus 7.8% based on piers II and III). The East Med became a maritime cul-de-sac due to the dramatic drop in Suez Canal transits. In the West Med and the Atlantic coast, Sines, Barcelona, and Valencia all recorded very robust growth. Gioia Tauro in the central part of the Med also achieved a double-digit growth last year. Nearby Marsaxlokk advanced 2%. Container traffic in the Spanish transshipment hub of Algeciras stagnated, struggling against strong competition from the rapidly growing Tanger Med on the opposite side of the Strait of Gibraltar, which handled 10.24 million TEU in 2024 (+18.8%). Las Palmas falls outside the top 15 but is gradually closing in on Marseille with a total TEU throughput of 1.32 million TEU in 2024.

The Benelux ports of Rotterdam and Antwerp-Bruges remain the largest container ports in the EU by a significant margin. The TEU gap between the top 2 and Hamburg widened to about 6 million TEU. Valencia overtook Piraeus to become the fourth largest EU port in 2024 and about 2.3 million TEU from Hamburg’s volume. Algeciras and Piraeus have comparable TEU figures closely followed by Bremerhaven, Gioia Tauro and Barcelona. The French HAROPA gained two places to reach the tenth position in the ranking“.