By Theo Notteboom

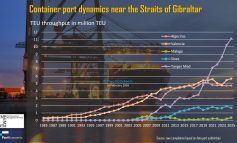

The Straits of Gibraltar is strategically located on some of the most important East-West trade lanes. Ports in the wider region around the Straits have good reasons to convince shipping lines of making a call at their container terminal facilities for transhipment and interlining purposes. Algericas at the southern tip of the Iberian Peninsula was the first to reap the benefits of its geographical location. Its share in the total volume handled by the five ports considered in the graph reached close to 70% in the mid-1990s, but this share gradually dropped to some 35% in 2014. Still, Algeciras is the largest container port in the Med with a volume of 4.55 million TEU with some 95% of its throughput related to the transhipment business. Valencia initially developed as a gateway port, but later on developed a keen interest in the transhipment business as well, mainly as a result of the activities of MSC. Handling 4.44 million TEU in 2014, Valencia is the second largest Med port combining an important gateway function with significant transhipment flows. In the early 2000s, Malaga started to draw attention as a potential transhipment location. The port managed to boost volumes to about 542,000 TEU in 2007, but in 2014 throughput fell to approximately 100,000 TEU.

Sines in Portugal and Tanger Med in Morocco are the new kids on the transhipment business block. Both ports have managed to significantly increase their share in the past five years: Sines from 2.7% in 2008 to 9.2% in 2014, Tanger Med from 10.7% in 2008 (the year after the opening of the first terminals) to 23% in 2014. MSC has a strong presence in Sines, a port which is particularly keen on developing a turntable position in the trade between Asia, Europe and South America. The growing container terminal market in the Maghreb countries increases competition in the Med region. Tanger Med is hoping to bring in dividends from factory delocalization movements to Maghreb countries, particularly to Morocco. The objective is to start stopping vessels from Asia for attracting cargo and partially deviating container volumes from traditional European ports. In addition, the launching of Free Trade Zones (FTZ) initiatives like in Tangier (Morocco) might stimulate local economic growth and attract foreign direct investments, thus boosting additional traffic growth.

The real challenge for the transhipment hubs in the region might however come from elsewhere. Container lines are reconfiguring their global shipping networks and are paying more and more attention to direct services between Asia and West/Southern Africa, and Asia and South America. These trades now typically use the Suez route with interlining activity near the Straits of Gibraltar or even in one of the large north European ports such as Antwerp and Rotterdam. The growing south-south trade has already led to the introduction of direct container services passing via the Cape route making interlining via the European and North African hubs redundant. The south-south route via the Cape presents a distance and transit time advantage compared to the Suez route (*). Vessel sizes on the Cape route are also on the rise, narrowing the difference in scale economies compared to the Suez route. It is clear port competition is outgrowing the regional level.

(*) See also Notteboom, T. (2012), Towards a new intermediate hub region in container shipping? Relay and interlining via the Cape route vs. the Suez route, Journal of Transport Geography, Volume 22, pp. 164-178