By Theo Notteboom

By Theo Notteboom

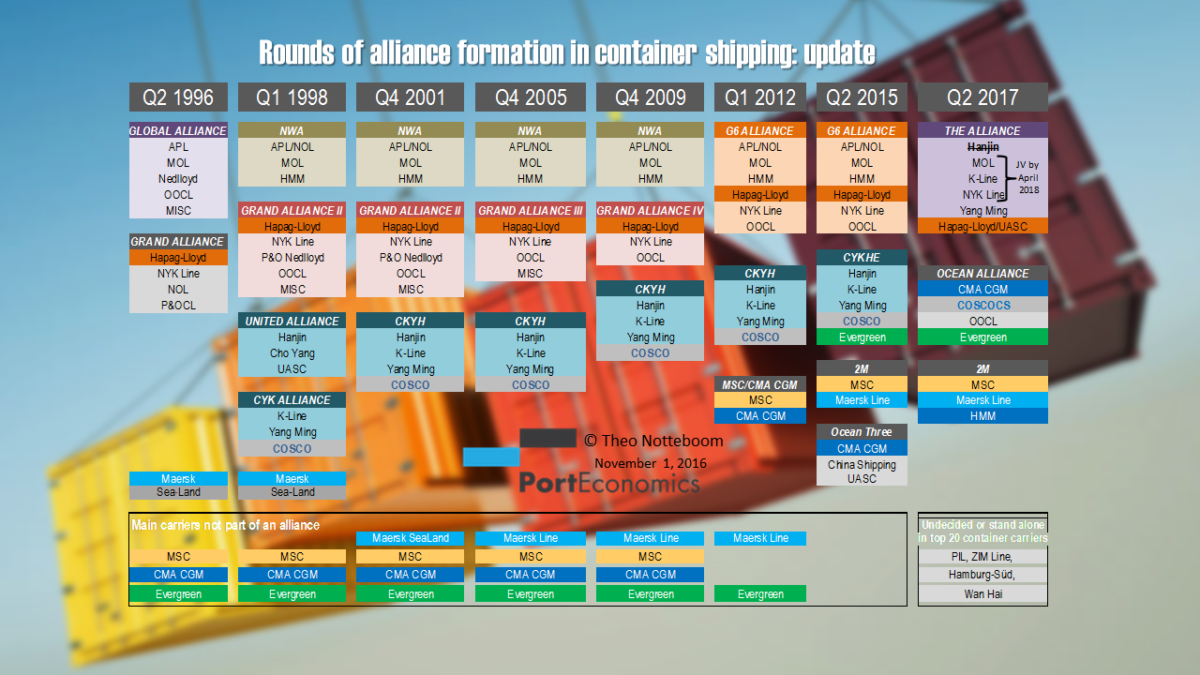

Since 2015 four alliances are operational in the container shipping market: 2M, Ocean Three, CKY(H)E and G6. The merger of China Shipping and Cosco to form China Cosco Container Lines (COSCOCS) and the acquisition of APL/NOL by CMA CGM were the first major market changes signalling major changes in the current alliance structure. By Q2 of 2017, the new alliance landscape would include the 2M alliance and two new large-scale alliances, i.e. the Ocean Alliance and THE Alliance.

In the past few months the container shipping market underwent another round of major changes primarily affecting THE Alliance. First, Hapag-Lloyd and UASC have integrated their liner shipping activities implying that UASC de facto became part of the planned THE Alliance albeit under the Hapag-Lloyd banner. Second, the Korean and Japanese container scene is undergoing major transformations. Hanjin filed for bankruptcy, resulting in one member less for THE Alliance. Its Korean colleague Hyundai Merchant Marine (HMM) announced to join the 2M Alliance. And today Japanese carriers K-Line, MOL and NYK announced that they are planning (subject to regulatory approval) to establish a new joint-venture company which would integrate the container shipping businesses and global terminal operating businesses of all three companies (on a 31/31/38% basis respectively). The company will be established by July 1, 2017 and will become operational by April 1, 2018. It is yet unclear whether this new event might have an impact on the planned THE Alliance, although we have to consider that all three Japanese carriers previously announced to take part in THE Alliance.

The graph clearly shows that strategic alliances are never lasting and thus subject to change. The intensity of the latest round of carrier reshuffling demonstrates that the current market conditions make individual shipping lines show an increased level of pragmatism when setting up partnerships with other carriers on specific trade routes.