By Theo Notteboom

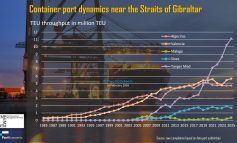

In 2014, 23.4% of the total European container port traffic was handled by Belgian and Dutch ports. With these figures, the Rhine-Scheldt Delta port region, which includes all Dutch and Belgian ports, is the most important port region in Europe – and PortEconomics co-director Theo Notteboom discusses the “Holland vs. Belgium” match in the container business:

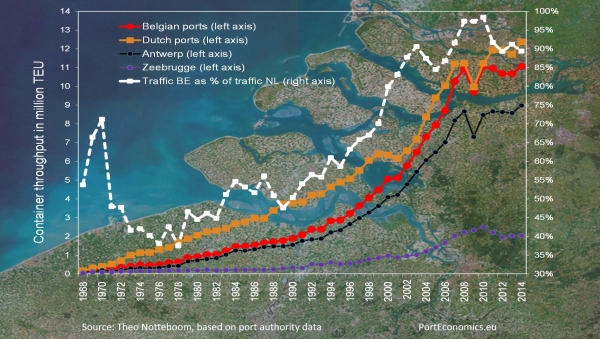

“In the late 1970s, Dutch ports handled three times more containers than Belgian ports. The graph demonstrates that the combined container volumes in the Belgian ports of Antwerp and Zeebrugge closed in fast on Dutch ports during the 1990s and the early 2000s. In 2010 the gap was almost closed, but in more recent years the traffic difference stabilized at around 10%. Rotterdam dominates the Dutch port system handling about 99.5% of all Dutch container port traffic.

Just before the crisis, Amsterdam’s container business saw a temporary rise, but Rotterdam’s share in total Dutch throughput never dropped below 98.6%. The Belgian container port system relies on two ports: upstream port Antwerp and coastal port Zeebrugge. Antwerp is the third largest container port in Europe after Rotterdam and Hamburg. The Belgian port of Zeebrugge initially overcame the crisis very well (even becoming the ninth largest container port in Europe in 2010), but afterwards booked traffic losses pushing the seaport back to position 13.

The Rhine-Scheldt Delta port system has one of the largest terminal capacity reserves in Europe. The massive Deurganck dock in the port of Antwerp, which opened in 2005, will soon welcome an upscaled MPET, a joint venture terminal of MSC and PSA now still located at the Delwaidedock on the right bank. A deepening program of the river Scheldt was completed a few years ago in view of guaranteeing access to the largest container vessels within an acceptable tidal window. The current Maasvlakte 2 developments in Rotterdam include the construction of two large scale container facilities, each with a capacity of between 4 and 5 million TEU when fully developed: a terminal for APM terminals and the Rotterdam World Gateway which will be operated by a consortium led by DP World. The first phases of both terminals come on stream this year. ECT, part of Hong Kong based Hutchison Port Holdings, has room for further capacity growth by extending the current 1.5 km quay of its Euromax terminal. The terminal capacity in Zeebrugge is at the eve of a major reconfiguration involving PSA’s OCZ terminal, PSA’s new and hardly used Zeebrugge International Port (ZIP) facility and the APM Terminals facility in the outer harbour.

The strong hinterland ambitions of the Rhine-Scheldt Delta ports are supported by a range of hinterland concepts and products such as a strong orientation on barge transport, a growing momentum for rail shuttles into the distant hinterland, ECT’s European Gateway Services network and similar efforts by DP World and PSA, and a dense network of inland terminals and European distribution zones in or in the vicinity of the ports. To secure growth in the future, the ports are actively targeting transhipment markets in the Baltic, the UK and southern Europe and hinterland areas in southern Germany, Italy, South France (cf. Lyon area) and Eastern and Central Europe, next to a continued focus on their cargo rich core service areas (the Benelux, western Germany and northern France)”.